Updated:

Readtime: 17 min

Every product is carefully selected by our editors and experts. If you buy from a link, we may earn a commission. Learn more. For more information on how we test products, click here.

- The electric vehicle market share reached a record 23.3 per cent in June.

- Tesla’s Model Y holds an absolute sales lead across the country.

- New platforms from BYD, Geely, and Zeekr recorded major volume gains.

- Sub-forty-thousand-dollar options account for multiple leaderboard positions.

- Mid-sized electric SUVs remain the clear preference for local buyers.

Despite a global shift away from pure battery electric vehicle (BEV) models, the market here in Australia tells a completely different story. With our exposure to Chinese models and a race to the bottom on price in a bid to own market share, it seems we’ve finally moved beyond early adoption and into high-stakes, volume-driven mass competition. Over the first half of 2026, pure electric models captured a record share of national vehicle deliveries, driven also by severe cost-of-living pressures and a collective consumer choice to reduce exposure to volatile fuel prices.

With direct factory-to-consumer logistics pipelines now established, dedicated vehicle-shipping operations now in place, and a wave of fresh mid-sized arrivals entering local showrooms, the zero-emission leaderboard has completely transformed.

While traditional combustion segments are cooling off in line with mandated emissions regulations, electric vehicle sales have grown, and consumer migration toward pure-electric layouts is stabilising as a permanent shift in buying habits. Now that we are halfway through the year, let’s look at how the top-selling battery electric car models in Australia stack up and see which brands are leading the pack.

Most Popular Electric Cars in Australia at a Glance

These are Australia’s most popular pure electric vehicle models halfway through the year, according to official data from the Electric Vehicle Council (EVC) and the Federal Chamber of Automotive Industries (FCAI).

| Rank | Model | 2026 YTD Sales | Segment Type |

| 1 | Tesla Model Y | 20,396 | Medium SUV |

| 2 | BYD Sealion 7 | 12,516 | Medium SUV |

| 3 | Geely EX5 | 6,756 | Medium SUV |

| 4 | Zeekr 7X | 5,532 | Medium SUV |

| 5 | BYD Atto 2 | 5,401 | Small SUV |

| 6 | BYD Atto 1 | 3,254 | Light Hatchback |

| 7 | MG MG4 | 3,252 | Small Hatchback |

| 8 | Tesla Model 3 | 3,192 | Medium Sedan |

| 9 | BYD Atto 3 | 3,052 | Medium SUV |

| 10 | Kia EV5 | 2,951 | Medium SUV |

1. Tesla Model Y

Total number of sales in H1 2026: 20,396

The Tesla Model Y holds the top spot as the best-selling EV by a significant margin, with 20,396 deliveries in the first six months of the year. This volume places the mid-sized crossover as the third-most-popular vehicle platform overall in the country, tracking ahead of high-volume traditional alternatives like the Toyota RAV4. We recently spent a week validating its highway efficiency and upgraded damping structures in our Tesla Model Y Performance review, plus we put the brand’s latest driving assist suites to the test when we evaluated Tesla Full Self-Driving Supervised on Australian roads. Ultimately, it was the newly introduced Model Y L that helped sales the most, and while they haven’t broken that model down separately in the data, it’s given the brand the sales injection it needed.

Key specifications for the Tesla Model Y:

- Price: from AUD$58,900 (before on-road costs)

- Range: 455km – 580km (WLTP)

- Power: 220kW – 343kW

- Drivetrain: Rear-wheel drive / All-wheel drive

2. BYD Sealion 7

Total number of sales in H1 2026: 12,516

BYD’s mid-sized Sealion 7 SUV has continued to gain traction in the market, securing second place with 12,516 units sold. Positioned as a direct competitor to the Model Y, the coupe-styled SUV has quickly established itself as the primary volume driver for the brand’s local operations. The reality is that most of these mid-size electric SUVs are much of a muchness, but BYD’s competitive advantage is that its direct factory production lines (including its own cargo ship) have helped the model pull buyers towards the brand, as it’s immediately available. Sure, it’s a year and a half old now, but it’s still a worthy, larger alternative to the brand’s smaller passenger variants, such as the Atto 1 and Atto 2.

Key specifications for the BYD Sealion 7:

- Price: from AUD$54,990 (before on-road costs)

- Range: 456km – 482km (WLTP)

- Power: 230kW – 390kW

- Drivetrain: Rear-wheel drive / All-wheel drive

3. Geely EX5

Total number of sales in H1 2026: 6,756

The return of the Geely brand to the market (it was previously sold as a Western Australian exclusive a decade ago) relies heavily on the EX5 mid-sized SUV, which ranked third on our list of the top-selling EVs in Australia, with 6,756 sales through June. Built on a dedicated electric architecture, the EX5 targets family buyers seeking maximum cabin space and tech on a budget while avoiding the higher price points of established segment options.

Despite its compact physical footprint, measuring 4,615mm in overall length, the EX5 offers a 410 litre rear boot that expands to 1,877 litres with the rear seats folded flat. While it trails the outright cargo limits of the slightly longer 4,750mm Tesla Model Y (which leads the class with an 854-litre seats-up capacity), the Geely matches up aggressively on cabin floor usability against more expensive, swooping silhouettes like the 4,830mm BYD Sealion 7, which offers a 500-litre rear boot.

However, it might be hard for some to look past the dynamic compromise of the EX5’s front-wheel-drive layout. Unlike the rear-wheel or all-wheel-drive configurations standard on both the Model Y and Sealion 7, the front-drive Geely can struggle to deploy its 160kW of power in the wet, proving far too eager to spin up its unloaded front wheels when you lean on that instant electric torque.

Key specifications for the Geely EX5:

- Price: from AUD$41,990 (before on-road costs)

- Range: 450km – 475km (WLTP)

- Power: 160kW

- Drivetrain: Front-wheel drive

4. Zeekr 7X

Total number of sales in H1 2026: 5,532

We’ve spent quite a bit of time behind the wheel of the Zeekr 7X since its launch, and it’s clear we were right about its potential, as it has mounted a firm challenge in the upper electric tiers, with 5,532 units sold so far this year. While the BYD and Tesla sit closer to the $60,000 price point, this mid-sized SUV takes things up a notch to the premium segment around the $70,000 threshold by pairing fast-charging architecture and high equipment lists with a great real-world driving range.

Measuring 4,787mm in total length and underpinned by Geely’s modular Sustainable Experience Architecture (SEA) platform, the 7X rides on a 2,900mm wheelbase that prioritises rear-seat space. Practicality-wise, its rear cargo area offers a 539-litre capacity that expands to 1,978 litres when the seats are folded flat, supplemented by a handy 62-litre frunk under the bonnet, where we stored the charging cables during our test.

While the standard seats-up storage capacity falls short of the Tesla Model Y’s class-leading limits, Zeekr counters by being one of the few EVs on the top-selling list, thanks to an advanced 800-volt electrical setup. This electrical architecture enables the standard 75kWh battery variant to complete a 10 to 80 per cent DC rapid top-up in as little as 13 minutes.

Key specifications for the Zeekr 7X:

- Price: from AUD$57,900 (before on-road costs)

- Range: 480km – 615km (WLTP)

- Power: 310kW – 475kW

- Drivetrain: Rear-wheel drive / All-wheel drive

5. BYD Atto 2

Total number of sales in H1 2026: 5,401

The compact SUV segment has seen a shift in volume with the arrival of the BYD Atto 2, which recorded 5,401 sales at launch. Positioned as one of the lowest-priced electric SUVs available locally, the model combines urban dimensions with technology to appeal to budget-conscious buyers. We originally covered its baseline placement alongside the brand’s luxury off-road initiatives when the BYD Atto 2 was confirmed for Australia, and now we can see its success in detail.

Measuring 4,310mm in total length and sitting on a compact 2,620mm wheelbase, the Atto 2 focuses explicitly on urban environments with its 5.25-metre turning radius. Best for smaller, younger families, it offers a 380-litre rear boot that expands to 1,320 litres with the rear seats folded down. While it falls short of the cargo volume of segment rivals like the Kia EV3, which offers a larger 460-litre boot, the BYD counters with a flat rear floor pan that delivers generous passenger legroom and headroom for adult occupants. However, the packaging has a minor practical drawback. Despite a massive void hidden beneath the bonnet where a front boot would naturally fit, it lacks a functional ‘frunk’ layout for tidy charging-cable storage.

Key specifications for the BYD Atto 2:

- Price: from AUD$31,990 (before on-road costs)

- Range: 345km (WLTP)

- Power: 130kW

- Drivetrain: Front-wheel drive

6. BYD Atto 1

Total number of sales in H1 2026: 3,254

Would you look at that, another BYD on the top-selling EVs list. It’s clear that BYD’s strategy of covering entry-level price brackets works and is best highlighted by the compact Atto 1 hatchback, which recorded 3,254 sales halfway through the year.

This model provides a simple layout aimed squarely at urban commuting and small households. When it was initially locked in for our local market, we broke down its specifications and its potential to be Australia’s cheapest EV. Measuring a diminutive 3,990mm in total length and sitting on a 2,500mm wheelbase, the Atto 1 pushes its wheels to the far corners of the chassis to carve out a good amount of cabin room from such a tiny footprint. Practically, the rear boot provides a cargo capacity of 308 litres and expands to 1,037 litres when the rear backrests are folded flat. While that seats-up storage volume is, as expected, compact compared to high-riding alternative crossovers, the deep floor space easily handles the normal suburban school-bag and grocery-run routine.

However, the primary compromise for this ultra-accessible entry threshold is that it’s strictly a four-seater. The dedicated 2+2 layout features a moulded centre console storage insert instead of a middle cushion and lacks a centre seatbelt entirely, meaning it cannot accommodate a third passenger across the back row if family duties call for it. It’s true that the 310km of range might be a deal breaker for many, so we recommend only looking at the Atto 1 if you plan on using it around town.

Key specifications for the BYD Atto 1:

- Price: from AUD$23,990 (before on-road costs)

- Range: 310km (WLTP)

- Power: 65kW

- Drivetrain: Front-wheel drive

7. MG MG4

Total number of sales in H1 2026: 3,252

While the brand has struggled for sales with greater competition, MG’s small hatchback line-up continues to show consistent sales momentum, recording 3,252 combined units across the first six months of 2026. The introduction of the MG4 EV Urban has helped, as the platform remains highly competitive among passenger car buyers by keeping final driving costs closer to internal-combustion alternatives. There remains a stock of the rear-wheel-drive model around, but this is what the future of the MG4 looks like, and the days of the face-melting performance bargain MG 4 XPower are over.

Measuring an elongated 4,395mm in total length (slightly longer than the standard 4,287mm hatch platform), the new MG4 EV Urban has switched to a front-wheel-drive layout, altering the car’s mechanical architecture to prioritise interior space and manufacturing efficiency. This front-driven packaging also expands the rear cargo bay to a larger 381-litre boot capacity that scales up to 1,266 litres when the rear backrests are folded flat. While this cargo capacity remains below that of high-riding alternative crossovers like the Geely EX5, it beats the previous generation’s 350-litre limit and, more importantly, the immediate budget competitor, the BYD Dolphin, which has a smaller 345-litre trunk.

However, there is a compromise, as moving the electric motor to the front axle means the Urban sheds the 50:50 weight distribution that we loved in the rear-drive MG4. Like many front-drive EVs, the car can occasionally scramble for traction under the instant torque of electric motors when pulling out of tight corners, but this dynamic trade-off is not something that buyers in this segment tend to care about. The update also brings a large 12.8-inch central touchscreen display and a welcome return of dedicated physical buttons for volume and climate controls, resolving prior menu-diving frustrations we had.

Key specifications for the MG MG4:

- Price From AUD$31,990 (drive-away)

- Range 316km – 405km (WLTP)

- Power 110kW – 118kW

- Drivetrain Front-wheel drive

8. Tesla Model 3

Total number of sales in H1 2026: 3,192

While its high-riding sibling claims the highest overall volume, the Tesla Model 3 sedan remains a prominent option for premium passenger car buyers, posting 3,192 deliveries. When we reviewed the revised sedan at launch, it matches long-range figures with sharp driving dynamics to contend with legacy premium mid-sized from the likes of BMW. It remains a compelling option, despite its unpopular sedan body style, trailing only slightly behind its larger Performance SUV stablemates in overall off-the-line acceleration as well.

Regarding practicality, the Model 3 features a 594-litre standard rear cargo layout that expands to a maximum combined total volume of 682 litres when utilising its deep underfloor cavity and the handy 88-litre front ‘frunk’ under the bonnet. While its slippery silhouette lets it extract significantly longer driving range figures from an identical battery pack compared to its taller crossover siblings (up to a massive 750km WLTP range in premium long-range setups), it only really yields outright cargo room to the larger 4,750mm Tesla Model Y and its class-leading 854-litre seats-up capacity.

Because it relies on a traditional hinged sedan trunk lid rather than a wide-opening rear liftgate hatch, we found that squeezing bulky, box-shaped family cargo into the rear aperture can be frustratingly restrictive. Furthermore, while the long wheelbase guarantees loads of passenger legroom, the sloping rear glass panel and slightly raised cabin floor pan mean taller adult occupants will find rear headroom significantly more pinched than in the high-riding Model Y or the boxier Kia EV5.

Key specifications for the Tesla Model 3:

- Price: from AUD$54,900 (before on-road costs)

- Range: 513km – 629km (WLTP)

- Power: 208kW – 343kW

- Drivetrain: Rear-wheel drive / All-wheel drive

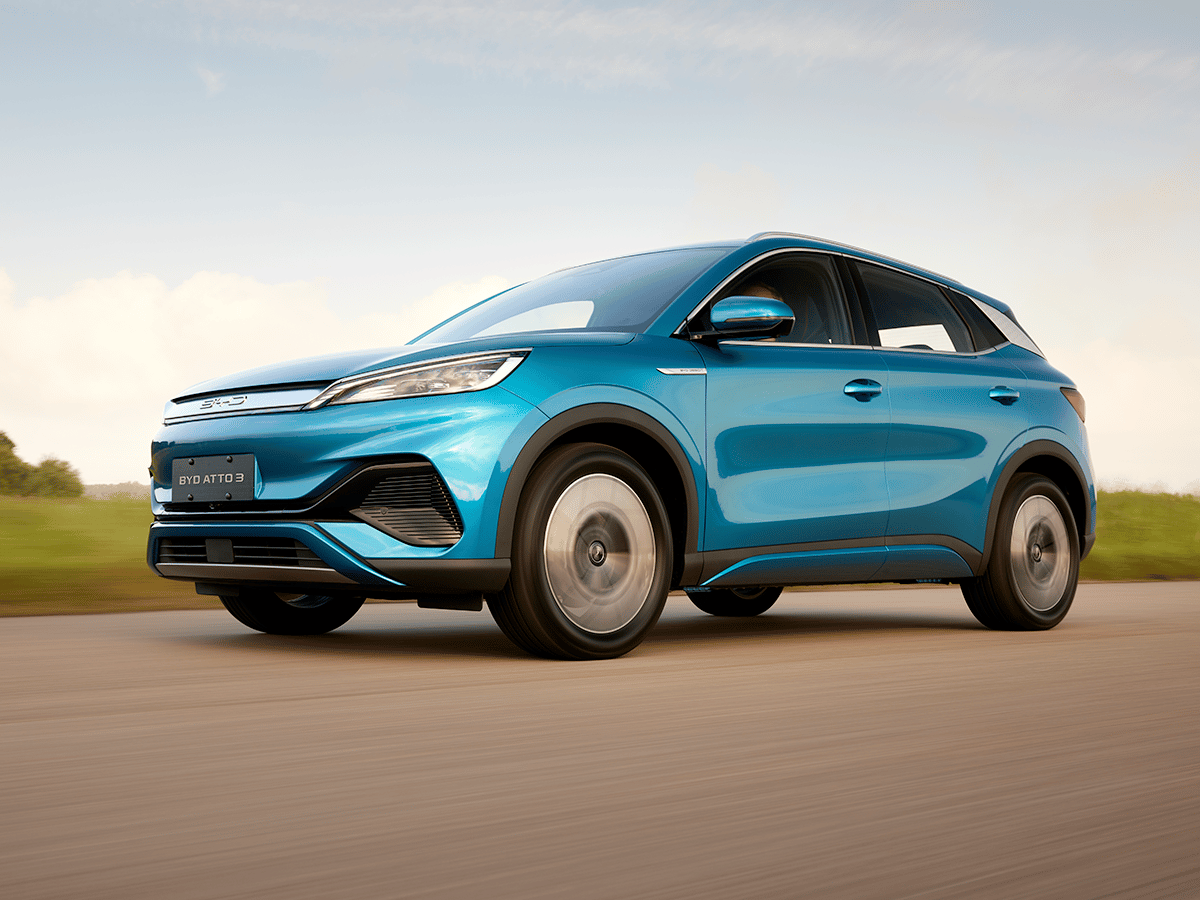

9. BYD Atto 3

Total number of sales in H1 2026: 3,052

The vehicle that launched BYD’s local line-up remains a steady performer, with the Atto 3 capturing 3,052 deliveries. While the arrival of the smaller Atto 2 has absorbed some of its prior volume momentum, the unique cabin styling and rotating central multimedia display keep it firmly anchored in the national top-sales mix for EVs. When we first reviewed the BYD Atto 3 years ago, we lauded it as a sensible family crossover packed with value, but much has changed since then, and plenty of competitors have entered the fold.

Measuring 4,455mm in total length and sitting on a 2,720mm wheelbase, the Atto 3 uses its dedicated EV architecture to optimise cabin floor space. It provides a standard 440-litre rear cargo layout that expands to 1,338 litres with the split-fold rear backrests packed flat. While that seats-up capacity is naturally more compact than larger mid-sized options like the Tesla Model Y or the brand’s own Sealion 7, its dual-level adjustable floor lets owners separate daily items from bulkier luggage. It’s worth noting the omission of a front ‘frunk’ storage compartment under the bonnet, meaning high-voltage charging cables must share space with family gear in the back.

Like the smaller Geely EX5, the Atto 3 relies on a standard front-wheel-drive motor configuration deploying 150kW. This means under sudden acceleration, the front tyres can scramble for traction as instant electric torque shifts weight away from the front axle. Still, not many are buying this vehicle for its dynamics.

Key specifications for the BYD Atto 3:

- Price: from AUD$44,490 (before on-road costs)

- Range: 345km – 420km (WLTP)

- Power: 150kW

- Drivetrain: Front-wheel drive

10. Kia EV5

Total number of sales in H1 2026: 2,951

Kia completes the top-selling EVs list with its mid-sized EV5 SUV, recording 2,951 customer handovers. By implementing an advanced, dedicated electric platform with multiple battery options, the Korean manufacturer has maintained its base sales amid a growing pool of new competitors. It stands as an important visual buffer for the brand as buyers migrate away from small traditional hatchbacks in favour of larger SUVs of varying sizes.

Measuring 4,615mm in total length and sporting a boxy, upright silhouette, the EV5 prioritises spatial efficiency. Its squared-off rear end delivers a 513-litre standard boot capacity that expands to 1,714 litres when the second row is folded completely flat, supplemented by a generous 67-litre front ‘frunk’ beneath the bonnet, perfect for stowing wet charging cables out of the main cabin.

On the move, standard and long-range variants are front-wheel drive, utilising a 160kW motor. While it swaps the rear-driven handling of the Model Y for a relaxed, comfort-oriented commute, the instant torque requires smooth inputs to prevent the front axle from breaking traction on damp city streets.

Key specifications for the Kia EV5:

- Price: from AUD$56,770 (before on-road costs)

- Range: 400km – 555km (WLTP)

- Power: 160kW – 230kW

- Drivetrain: Rear-wheel drive / All-wheel drive

Why Every Top-Selling EV in Australia is Sourced From China

When we take a closer look at the sales leaderboard, it reveals a fascinating, unifying trend. Every single one of Australia’s most popular electric vehicles is manufactured in China. The clear sweep highlights an industrial shift in the local automotive market, proving that dominance in the electric era is no longer determined by a brand’s corporate headquarters, but by the efficiency of its global supply chain, and the price it can sell its vehicles at, all in a bid to capture market share before the next player turns up.

While Chinese marques like BYD, Geely, and Zeekr continue to aggressively expand their local footprints this way, established global badges have quietly shifted their electric operations to Chinese manufacturing hubs to keep retail pricing competitive. Tesla’s high-volume local deliveries of the Model Y and Model 3 rely entirely on production allocations clearing Gigafactory Shanghai. More significantly, the tenth-placed Kia EV5 marked a historical milestone as the first vehicle Kia Australia has ever sourced from a Chinese factory. More specifically, the brand’s joint-venture assembly lines in Yancheng, thereby bypassing the higher production costs of South Korean lines.

The logic driving this shift comes down to proximity to raw materials and battery technology. By building vehicles in the world’s most advanced EV ecosystem, these manufacturers enjoy direct access to high-volume Lithium Iron Phosphate (LFP) battery suppliers, including CATL and BYD’s FinDreams division. This advantage drastically reduces component transport times, insulates production from localised logistics issues, and provides automakers with the financial headroom to implement the aggressive price corrections currently reshaping Australian showroom floors.

What This Means for the Future of the Local EV Race

We wanted to take a break to look at the top-sellers halfway through the year, as we’re at a turning point for EV sales in the country. The mid-year registration numbers now indicate that the make-up of the local electric vehicle sector has entered a highly competitive lifecycle, marked by a sharp acceleration in volume in the second quarter. While the first three months of the year established a steady baseline, the market experienced a structural shift immediately after the close of Q1 as global forces began to take hold.

This post-March momentum represents a 144.7 per cent increase in monthly delivery between the end of March and the close of the half. This trajectory demonstrates that local appetite for battery-electric options is expanding rapidly, successfully shrugging off the supply lulls and port delivery bottlenecks that have throttled volumes in the past.

The other takeaway for us is that volume is no longer confined to a single market leader or legacy passenger form factors. Sure, Tesla will likely lead the pack for a while longer, but no one model is a road to success. Crossover utilities and budget-tier city models are moving into mainstream positions, demonstrating that long-term consumer interest relies almost entirely on maximising functional equipment while keeping standard retail pricing as low as possible. The manufacturers that successfully navigate domestic port processing times, scale their charging infrastructure, and maintain realistic driving dynamics will continue to dictate the terms of Australia’s automotive transformation towards electric vehicles. With NVES, it’s not a case of if, but when.

Comments

We love hearing from you. or to leave a comment.